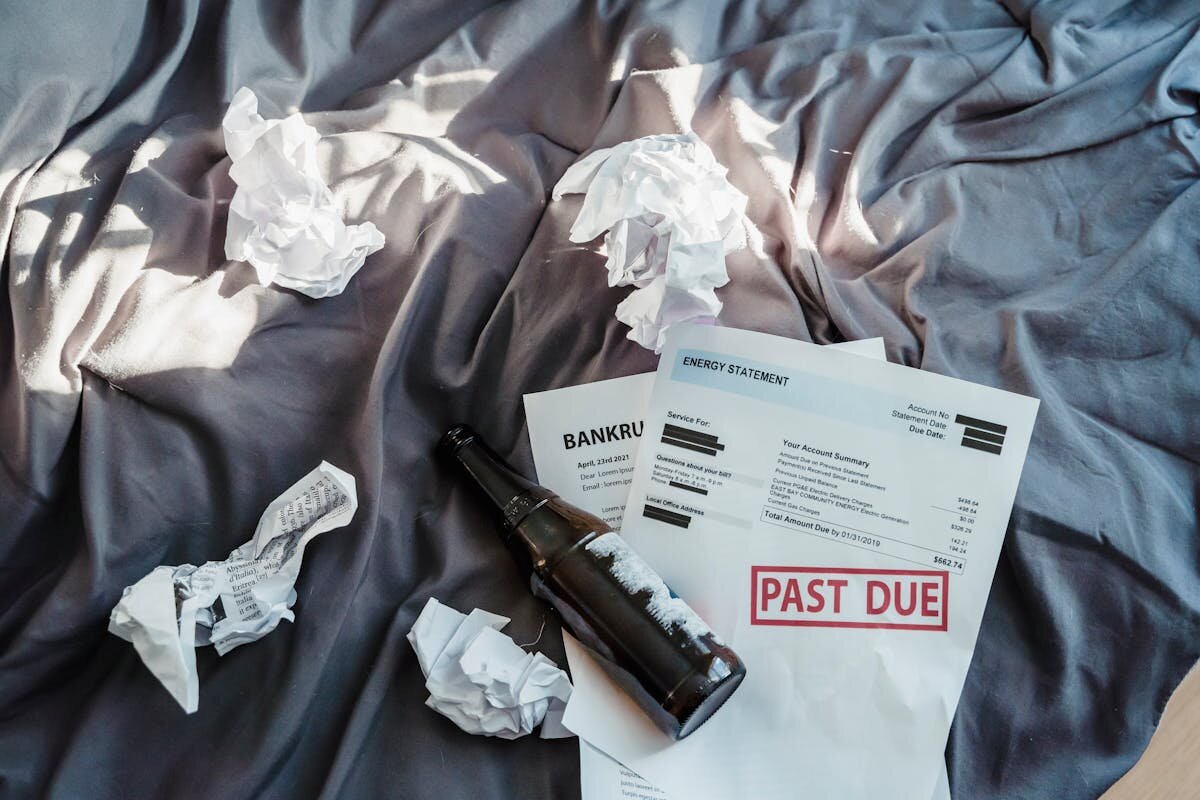

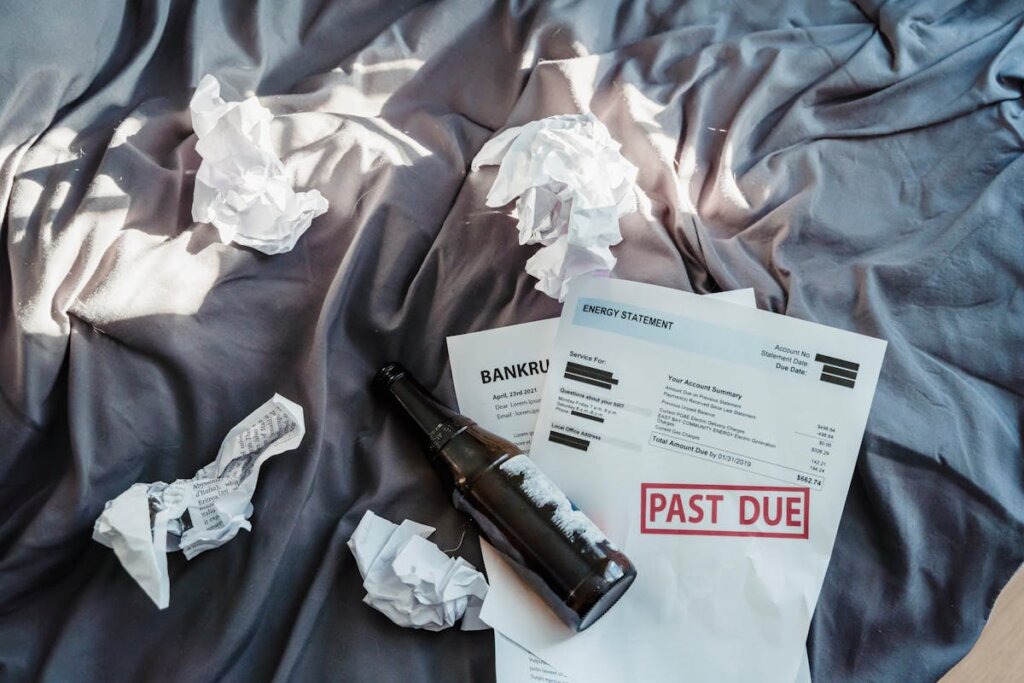

Navigating through bankruptcy is a challenging journey, and for many homeowners, selling a home afterward can seem like an additional layer of complexity. However, selling your home post-bankruptcy is possible, and with careful planning, you can streamline the process and achieve financial stability.

This guide will cover everything you need to know about selling a home after bankruptcy, offering tips to help make the process as smooth as possible.

Understanding Bankruptcy and Its Impact on Homeownership

Before diving into the specifics of selling a home post-bankruptcy, it’s essential to understand how bankruptcy affects homeownership. In the U.S., two types of personal bankruptcy are most common: Chapter 7 and Chapter 13.

- Chapter 7 Bankruptcy: Known as “liquidation bankruptcy,” Chapter 7 discharges most of your debts, but you may have to sell certain assets, including your home, unless it is exempt under your state’s laws.

- Chapter 13 Bankruptcy: Often referred to as a “wage earner’s plan,” Chapter 13 allows you to keep your property, including your home, while repaying debts over a set period, typically three to five years.

Both types of bankruptcy impact your credit score, but they do not necessarily prevent you from selling your home for cash. In fact, selling a home after bankruptcy can be an effective way to resolve remaining financial challenges and start fresh.

Tip 1: Confirm Eligibility to Sell

After filing for bankruptcy, your home may be part of the bankruptcy estate, meaning you can’t sell it without court approval or guidance from your bankruptcy trustee. Your first step should be to confirm whether you are eligible to sell the home.

- For Chapter 7 filers, if your home has been exempted from liquidation, you retain the right to sell it. However, if the home is not exempt and is part of the bankruptcy estate, you may need to wait until the bankruptcy proceedings are complete.

- For Chapter 13 filers, you can generally sell your home during the repayment period, but you must seek approval from the court and ensure that any proceeds are accounted for in your repayment plan.

Tip 2: Seek Professional Guidance

Selling a home post-bankruptcy requires expertise. You should consult both a bankruptcy attorney and a real estate professional experienced in these types of sales.

- Bankruptcy Attorney: A bankruptcy lawyer will ensure that you comply with all legal requirements. They can guide you through the necessary steps to get court approval if required and make sure you don’t inadvertently violate the terms of your bankruptcy.

- Real Estate Agent: An agent familiar with selling homes post-bankruptcy will know how to market your property while being sensitive to your unique financial situation. They can also help negotiate with buyers to ensure a fair price.

Tip 3: Improve Your Home’s Appeal

Even though you may be recovering from bankruptcy, making small improvements to your home can increase its market value and attract more potential buyers. Focus on affordable, high-impact changes:

- Fresh Paint: A fresh coat of paint in neutral colors can brighten the space and make it more appealing to prospective buyers.

- Basic Landscaping: Tidying up the yard and planting some low-maintenance greenery can significantly boost curb appeal.

- Decluttering: A clean, clutter-free home looks more spacious and inviting. Consider staging the home or rearranging furniture to show off its best features.

Tip 4: Be Transparent with Buyers

It’s essential to be upfront with potential buyers about your bankruptcy situation, particularly if it will affect the sale process. Full transparency can help avoid misunderstandings or delays down the line.

- Disclosures: In many states, you must legally disclose if your home is under any bankruptcy proceedings. Being honest about your financial situation can build trust with buyers, and some may even be willing to work with you to accommodate necessary delays or paperwork.

- Timeline: Let buyers know if you need extra time to get court approval for the sale, especially in Chapter 13 cases where trustee approval is required. While this may narrow the buyer pool slightly, serious buyers will appreciate the transparency and be more likely to work with you.

Tip 5: Price Your Home Competitively

Pricing is a critical factor in selling any home, but it becomes even more crucial when selling post-bankruptcy. Work closely with your real estate agent to set a price that reflects the current market while being realistic about your home’s condition. You could even sell your house for cash.

- Market Analysis: Your agent should conduct a comparative market analysis (CMA) to determine what similar homes in your area are selling for. This will help you avoid overpricing, which could cause your home to sit on the market longer.

- Fair Valuation: Depending on your home’s condition, you may need to price it slightly below market value to attract more buyers. However, avoid underpricing to ensure you get the most value out of the sale, which may help pay off remaining debts.

Tip 6: Consider Selling As-Is

If you’re unable or unwilling to make repairs or updates to the property, selling the home “as-is” can be a viable option. This is particularly useful if you need to sell quickly to pay off debts or complete the bankruptcy process.

- Attract Cash Buyers: Many investors and homebuyers are looking for homes they can purchase as-is, often paying cash and closing quickly. This can save you the hassle of repairs and shorten the sales timeline.

- Work with a Cash Home Buyer: Companies like Neighbor Joe specialize in buying homes as-is. They can provide a quick cash offer and eliminate the need for staging, repairs, or traditional buyer negotiations. This route can be ideal if you’re looking to move on from the property quickly after bankruptcy.

Tip 7: Be Prepared for Taxes and Fees

Selling a home post-bankruptcy can still result in taxes and fees that need to be addressed. Be sure to account for these costs so you are not caught off guard.

- Capital Gains Tax: Depending on how much you sell the home for and how long you’ve owned it, you may be subject to capital gains tax. However, primary residences have exclusions—up to $250,000 for single filers and $500,000 for married couples.

- Conveyance Tax: In states like Connecticut, real estate transfer taxes (or conveyance taxes) apply to most home sales. Factor this into your calculations to ensure you know how much you’ll owe at closing.

- Attorney Fees: If you require a bankruptcy attorney to assist with the sale, those fees will need to be paid as well. Keep this in mind when budgeting for closing costs.

Tip 8: Work on Rebuilding Credit

After selling your home and finalizing the bankruptcy process, your focus should shift to rebuilding your credit. A higher credit score will open doors to future opportunities, whether buying a new home or obtaining better loan terms for other purchases.

- Monitor Your Credit: Regularly check your credit report to ensure that your bankruptcy has been properly discharged and that no errors are negatively affecting your score.

- Consider Small Loans or Secured Credit Cards: Building credit through small, manageable loans or secured credit cards can gradually increase your score.

Conclusion

Selling a home after bankruptcy might seem daunting, but with the right approach, it can be a strategic step toward financial recovery. By following the tips outlined above—seeking professional help, improving your home’s appeal, being transparent, and considering your selling options—you can navigate this process with confidence.

Whether you choose to list your home traditionally or sell it as-is to a cash buyer like Neighbor Joe, remember that a smooth sale is possible even after bankruptcy.