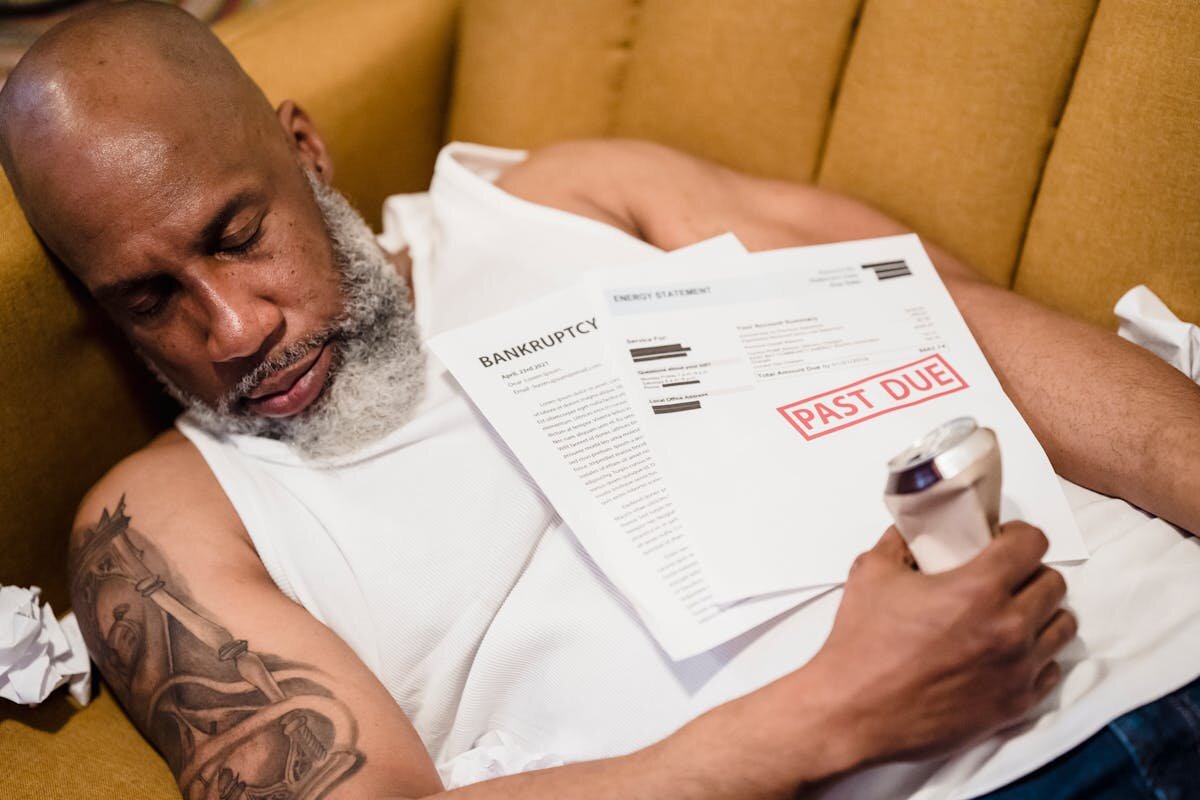

Financial hardship can hit suddenly and without warning. Whether it’s due to job loss, medical expenses, or other unexpected life events, the stress that follows can feel overwhelming—especially when you’re struggling to make mortgage payments. For Connecticut homeowners, falling behind on monthly mortgage payments often leads to one looming fear: foreclosure.

Foreclosure is the legal process through which your lender can reclaim your home after several missed payments. Once foreclosure proceedings begin, they move through the Connecticut court system, potentially ending with the forced sale of your home at a public auction. This not only results in the loss of your property but also severely damages your credit score and your ability to secure future housing or loans.

If you’re asking yourself, “How can I save my home from foreclosure?”—the good news is that there are still options available. Even after the legal process begins, there are several ways you can take control, stop the foreclosure, and protect your home and your financial future.

Step One: Face the Problem Early

The moment you miss a mortgage payment or realize you won’t be able to make the next one, it’s crucial to take action. Many homeowners fall into the trap of denial, hoping that the situation will resolve itself or improve on its own. But the truth is, the sooner you act, the more choices you’ll have. Waiting until the foreclosure notice arrives limits your options significantly.

In Connecticut, lenders typically don’t start foreclosure proceedings until you’re at least 90 days behind on payments. This gives you a small but critical window to contact your lender, assess your financial situation, and explore solutions. Open the letters from your lender, respond to their calls, and keep all communication lines open. The worst thing you can do is ignore them.

Step Two: Talk to Your Lender

Many homeowners are surprised to learn that lenders often prefer alternatives to foreclosure. Foreclosure is expensive, time-consuming, and burdensome for banks, too. That’s why many mortgage lenders are open to negotiating with you directly. You might qualify for options such as forbearance, loan modification, or a repayment plan that allows you to catch up on missed payments over time.

Forbearance can temporarily suspend or reduce your payments while you recover from a financial setback. Loan modifications may involve changing the interest rate, extending the term of your loan, or even rolling missed payments into a restructured loan. In either case, your lender may be able to offer you a solution that helps you stay in your home and avoid the long-term damage that foreclosure can bring.

If you’re unsure how to negotiate with your lender, Connecticut homeowners can reach out to housing counselors approved by the U.S. Department of Housing and Urban Development (HUD). These counselors provide free or low-cost services and can help you understand your rights and negotiate effectively.

Step Three: Evaluate All Alternatives

There’s no one-size-fits-all approach to stopping foreclosure. The right solution depends on your income, equity in the home, current expenses, and how far along the foreclosure process is. In some cases, a short-term hardship may allow for reinstatement, where you pay the total overdue amount in one lump sum to bring the loan current.

In other situations, homeowners consider refinancing if their credit hasn’t taken too much of a hit. This means replacing your current mortgage with a new one that offers more favorable terms and possibly lower monthly payments. However, refinancing can be difficult if you’re already behind.

If keeping the home is no longer realistic, selling before foreclosure can be the smartest financial move. This option allows you to avoid the negative credit consequences and gives you the chance to walk away with your equity intact. It’s also far less damaging to your future housing options than having a foreclosure judgment on your record.

At Neighbor Joe, we help homeowners in Connecticut who are in distress. If you’re thinking of selling to avoid foreclosure, we can step in with a fair cash offer and close in just days—giving you the relief and flexibility you need to reset your finances and start fresh.

Step Four: Consider a Short Sale

In cases where the home is worth less than the balance on your mortgage, your lender may agree to a short sale. This means selling your house for cash for less than what you owe, with your lender accepting the sale proceeds as full payment for the loan.

A short sale still negatively affects your credit, but not as much as a foreclosure. More importantly, you avoid eviction, court appearances, and the long, stressful timeline that judicial foreclosure brings. Lenders may also offer relocation assistance as part of the process.

To pursue a short sale, you will need to demonstrate financial hardship and submit a package of documents to your lender, including bank statements, income verification, and a hardship letter explaining why you’re unable to continue with your mortgage payments. Working with a professional buyer like Neighbor Joe or a real estate agent who understands the Connecticut foreclosure process can make the process smoother and faster.

Step Five: Sell to a Cash Buyer

If you’re facing foreclosure and looking for the fastest, most stress-free solution, selling your home to a cash buyer is often the best route. CT cash home buyers like Neighbor Joe purchase homes as-is, without the need for inspections, repairs, or real estate agent involvement. This eliminates delays and uncertainty, allowing you to sell on your timeline and settle your mortgage before the court finalizes the foreclosure.

A cash sale not only helps you avoid the legal and credit damage of foreclosure but also puts money in your pocket quickly. There’s no waiting for buyers to secure financing, no last-minute cancellations, and no hidden fees. You pick the closing date, and we take care of the rest.

For many Connecticut homeowners under financial pressure, this kind of direct sale provides peace of mind and a clear path forward.

Don’t Wait—Act Now

If you’re still wondering how to save your home from foreclosure, remember that the clock is ticking. Every day that passes reduces the number of options available to you. But with early action, informed decisions, and the right support, you can avoid the worst outcomes and reclaim control over your situation.

Neighbor Joe has helped homeowners all over Connecticut who were in similar situations. Whether you’re in the early stages of missed payments or already facing a court-ordered foreclosure date, we can provide honest advice, real solutions, and a fair cash offer for your home.

Get Help from Neighbor Joe

You don’t have to go through foreclosure alone. At Neighbor Joe, we understand the emotional and financial strain foreclosure brings. That’s why we’ve made it our mission to offer a better way out. We’ll visit your home, give you a fair cash offer within 24 hours, and close in as little as 7 days. There are no commissions, no hidden fees, and no need to fix or clean your home.

If you’re in financial trouble and looking for a way to protect your future, we’re here to help. Contact us today and let us show you how easy it is to avoid foreclosure and move forward with confidence.